The first acquisition teaches a buyer how deals work. The third or fourth teaches a harder lesson: buying practices at scale is not the same deal repeated. Risk compounds rather than averages, early shortcuts become systemic problems, and volume exposes every weakness that a single transaction let the buyer get away with.

This article is for the expansion buyer — the owner-operator building a group, the emerging platform, the DSO adding locations — on what changes when acquisitions become a program, and how to structure for it.

Why buying at scale is different

In a one-off acquisition, a mistake is a cost. In a platform, the same mistake is a template. An informal compliance arrangement at location one becomes the de facto policy at locations two through six. A loose associate agreement, copied deal after deal, becomes a portfolio-wide enforceability problem. The diligence corner cut once becomes the corner the organization always cuts.

This is the transition from deal-making to platform risk: informal practices do not scale, and legal risk multiplies across locations instead of diluting. The buyer’s job changes accordingly — from getting this deal closed to building a system that closes deals without accumulating hidden liabilities.

Where platforms fail first

Three failure points appear earliest and most often.

Integration breakdowns. The deal closes; the integration does not. Systems, employment terms, and clinical workflows stay fragmented, and the “platform” is actually a collection of practices that share an owner and nothing else — which buyers of the platform will eventually notice.

Compliance drift. Each location arrives with its own habits. Without active standardization, the platform’s compliance posture is its worst location’s, multiplied: corporate practice exposure, supervision inconsistencies, and documentation gaps that vary site by site.

Management overload. The owner who personally managed two locations cannot personally manage six. Platforms that scale acquisitions faster than management capacity convert every operational weakness into a compounding one.

Integration is not just operational

The under-appreciated point about integration: much of it is legal work. Employment enforcement — acquired associates’ agreements need to be enforceable and actually enforced, consistently across locations, or the covenants exist only on paper. Policy standardization — one employee handbook, one set of clinical protocols, one compliance program, adopted formally at each location rather than assumed. Cultural alignment — not a legal task, but a legal risk when it fails, because the practices that resist integration are the ones where undocumented exceptions accumulate.

A platform that treats integration as a checklist of IT and signage tasks is deferring its legal integration to the worst possible moment: the recapitalization, when someone else’s diligence team does it instead.

Staffing and associates at scale

Human capital risk concentrates as platforms grow. Non-compete enforceability varies with drafting, jurisdiction, and changing law — a portfolio of inconsistent covenants, inherited deal by deal, protects much less than its page count suggests. Compensation misalignment across locations breeds churn: associates compare notes, and the platform that pays differently for the same work at neighboring locations is funding its own turnover. Churn risk itself scales nonlinearly, because each departure at a location with thin clinical coverage is a revenue event, not an HR event.

The fix is standardization in the deal documents themselves: a consistent associate agreement adopted at acquisition, compensation frameworks designed platform-wide, and retention terms built into integration planning rather than improvised after closing.

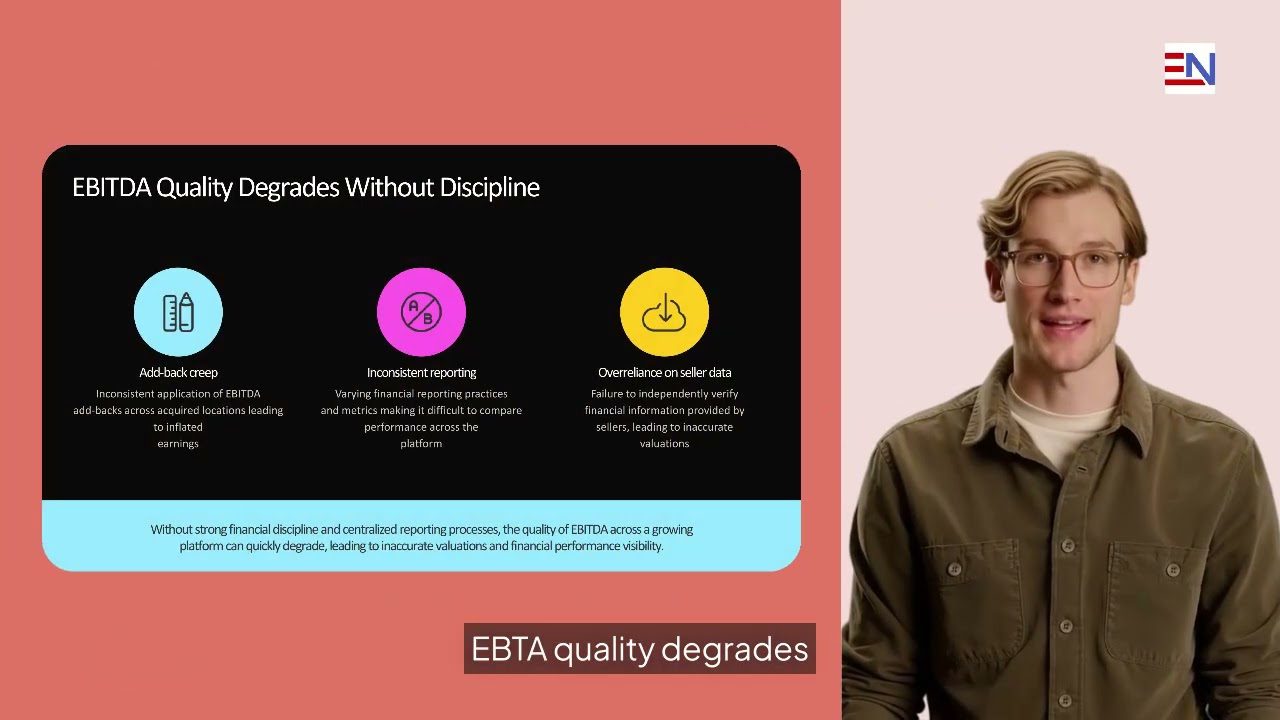

EBITDA quality degrades without discipline

A platform’s reported earnings are only as good as its weakest reporting. Three patterns erode EBITDA quality across growing groups: add-back creep, as each acquisition’s optimistic adjustments survive into platform reporting; inconsistent reporting, where locations keep their legacy bookkeeping and the consolidated numbers paper over the differences; and overreliance on seller data long after closing, because nobody rebuilt the location’s financials on the platform’s standards.

This matters twice. It distorts the platform’s own acquisition decisions — a buyer pricing deals against degraded internal numbers is compounding the error. And it surfaces, expensively, at recapitalization, when a quality-of-earnings review re-prices the whole platform against the numbers the platform should have kept all along.

Diligence fatigue is real

Repeat acquirers develop a specific vulnerability: diligence fatigue. The fifth deal looks like the fourth, the team is stretched, and “looks good enough” replaces review. Shortcutting becomes rational-feeling precisely because nothing went wrong the last time the shortcut was taken.

The defense is not heroic attention; it is process. Standardized diligence checklists that do not flex with the team’s energy level, defined no-skip items, and a decision record for each deal. Fatigue defeats vigilance; it does not defeat checklists.

Why standard forms stop working

Ironically, while diligence should standardize, deal documents standardize badly if done naively. One-size-fits-all asset purchase agreements fail because they ignore location-specific risk: the lease terms unique to this landlord, this location’s payor concentration, this seller’s transition role, this state’s or municipality’s regulatory quirks.

The right architecture is a disciplined template with engineered variation: a standard APA core that embodies the platform’s risk positions, plus a defined set of location-specific schedules and adjustments. Repeatability where the deals are alike; tailoring where they are not — and a clear understanding of which is which.

Integration timelines and hidden operational risk

Integration timing fails in both directions: too fast to absorb (staff loss, patient attrition, clinical disruption) and too slow to standardize (compliance drift hardens, legacy systems entrench). The pattern that works is a defined integration window — operationally, roughly the first ninety days — with named accountability for each workstream, followed by a longer standardization tail handled deliberately rather than by drift.

Meanwhile, three legal risks hide in routine operations across acquired locations and compound quietly: employment misclassification (contractor-classified associates and hygienists who fail the tests), improper delegation (procedures performed beyond what supervision rules permit), and HIPAA exposure (each location’s informal handling of patient data, multiplied). None of these announces itself; all of them surface in the platform’s eventual diligence, as deductions.

Private equity versus operator risk tolerance

Platforms answer to different masters. Private equity-backed buyers and owner-operators differ systematically: different time horizons (a fund’s exit clock versus an operator’s career), different enforcement priorities (a fund’s litigation budget and appetite versus an operator’s community relationships), and different exit pressure (a recap deadline changes which risks are acceptable today).

Neither posture is wrong, but deal structure should match the platform’s actual constitution. An operator who buys like a fund — or a fund-backed group that documents like a solo operator — has a strategy mismatch that diligence will eventually price.

Speed costs more later — and the exit proves it

The growth-at-all-costs pattern has a specific bill: deferred compliance costs that come due all at once, litigation risk from the corners cut in employment and covenant enforcement, and valuation haircuts at recapitalization when the buyer-of-the-buyer’s diligence surfaces the platform’s history.

That last point reframes everything. Every platform is eventually on the sell side. Preparing for recap or exit means assuming that a sophisticated acquirer will scrutinize the entire acquisition history — every APA, every compliance program, every integration. Buyer-of-the-buyer diligence finds what the platform’s own diligence skipped, and historical risk surfaces at exactly the moment it is most expensive. The platforms that command premium multiples are the ones that were built, from the early deals, as if that scrutiny were coming. It is.

What buyer-side counsel does at scale

For a platform, counsel’s role shifts from negotiating deals to systematizing them: building the risk review into a repeatable process, maintaining deal discipline when fatigue and momentum push against it, and protecting platform value — which means treating every acquisition’s legal work as an input to the eventual exit multiple, not just a closing checklist.

A scalable, buyer-protective platform looks the same from inside and outside: consistent compliance across locations, predictable integration, and a defensible valuation built on numbers the platform actually controls.

The deal kit: what repeat acquirers should standardize

For buyers ready to act on this, the practical artifact is a deal kit — built after the first or second acquisition and refined with each one. Its core components: a standardized diligence checklist with defined no-skip items; the platform’s APA template with its negotiated risk positions and a documented list of which provisions flex by location; the standard associate agreement and employee handbook adopted at every closing; a ninety-day integration plan template with named workstream owners; and a post-closing compliance audit that runs at each location on a schedule, not on suspicion.

The kit is not bureaucracy; it is the mechanism that converts the first deal’s lessons into the fifth deal’s defaults. It is also, not incidentally, exactly the documentation a recapitalization buyer’s diligence team hopes to find — and prices accordingly when it does.

The takeaway

Buying dental practices at scale rewards exactly one thing: systems that hold up under repetition. Fix the internal machinery before adding volume, standardize what should be standard, tailor what should not be, and treat legal risk as a strategic asset — because at recapitalization, that is precisely how it will be priced.

The full webinar deck, Buying Dental Practices at Scale, is available as a PDF download.

If you are building a group — or preparing an existing platform for its next acquisition or its eventual exit — conversations are confidential and focused on your specific goals. Schedule a confidential consultation.

This article is for informational purposes only and is not legal advice. No attorney-client relationship is formed by reading it.