In a dental practice sale, there is a brief window when the seller holds more leverage than they will ever hold again: the days before the letter of intent is signed. The buyer is competing, the market is open, and every term is still negotiable. The moment the LOI is signed, all three of those things begin to expire.

Most sellers treat the LOI as a formality on the way to the “real” documents. That ordering is backwards. The LOI sets the deal’s momentum, most of the seller’s leverage exists at this stage, and the later documents rarely fix LOI mistakes — they inherit them.

The misconceptions that cost sellers

Three beliefs about LOIs do consistent damage.

“It’s non-binding.” Parts of it usually are. But the standard LOI contains genuinely binding provisions — exclusivity, confidentiality, sometimes cost allocation — and the “non-binding” economic terms are practically binding even when they are not legally so. Walking a signed LOI’s price back up is rare; negotiating it down, as buyers know, is routine.

“We’ll fix it later.” Later, the seller’s market exposure is gone, exclusivity is running, and the buyer controls the timeline. Terms conceded at the LOI stage do not get clawed back in the asset purchase agreement; the APA is drafted to implement the LOI, not reopen it.

“This is just a formality.” The LOI determines the purchase price structure, the diligence scope, the exclusivity terms, and frequently the seller’s post-closing employment framework. Nothing else the seller signs before closing decides as much per page.

What an LOI actually does

Three functions, each with consequences.

It locks economic terms. Price, structure, and the major contingencies are fixed in the parties’ expectations from this point forward. It shapes diligence scope. What the buyer will examine, for how long, and with what access gets framed here. It sets expectations for the final deal. Courts aside, deal psychology treats the LOI as the agreement; deviations from it require justification, and the party requesting the deviation pays for it in goodwill or terms.

Binding versus non-binding provisions

Knowing which parts of an LOI bind is not academic. Typically binding: exclusivity and no-shop clauses, confidentiality, and cost allocation provisions. Typically non-binding: the economic terms — price, structure, closing conditions.

Note the asymmetry. The provisions that bind are the ones that constrain the seller (exclusivity, confidentiality); the provisions that do not bind are the ones that protect the seller (the price). A seller who signs a standard LOI has given binding commitments in exchange for non-binding ones. That trade can still be worth making — but it should be made knowingly, and the binding provisions should be negotiated with the same care as the price.

The economic terms set at the LOI stage

The LOI fixes more than a number. Purchase price structure — how much cash, when. Cash versus rollover equity — in DSO deals, the rollover percentage and its basic terms are usually established here. Earn-outs and holdbacks — contingent consideration and its conditions enter the deal at this stage, often in a single sentence that later becomes ten pages of the APA.

And price alone misleads. Structure determines risk; deferred consideration changes value; net proceeds matter more than headline price. Two LOIs with the same number on top can describe deals hundreds of thousands of dollars apart in expected value. The LOI stage is when that comparison can still change the outcome.

Exclusivity: the silent leverage killer

The exclusivity provision deserves its own section, because it is the single most underestimated term in the document.

A no-shop clause takes the seller off the market — the seller’s competitive leverage, which is most of the seller’s leverage, is suspended for the exclusivity period. The clock then works for the buyer: as weeks pass, the seller’s alternatives go stale, transaction fatigue builds, and re-marketing the practice after a failed exclusivity period means explaining to the next buyer why the last one left.

Exclusivity is a normal and reasonable buyer request; no serious buyer spends diligence money without it. The negotiation is about scope: how long, with what milestones, and what ends it early. Sixty days with diligence milestones is a different concession than 120 days without them. Sellers should price exclusivity like the valuable asset it is — because the buyer certainly does.

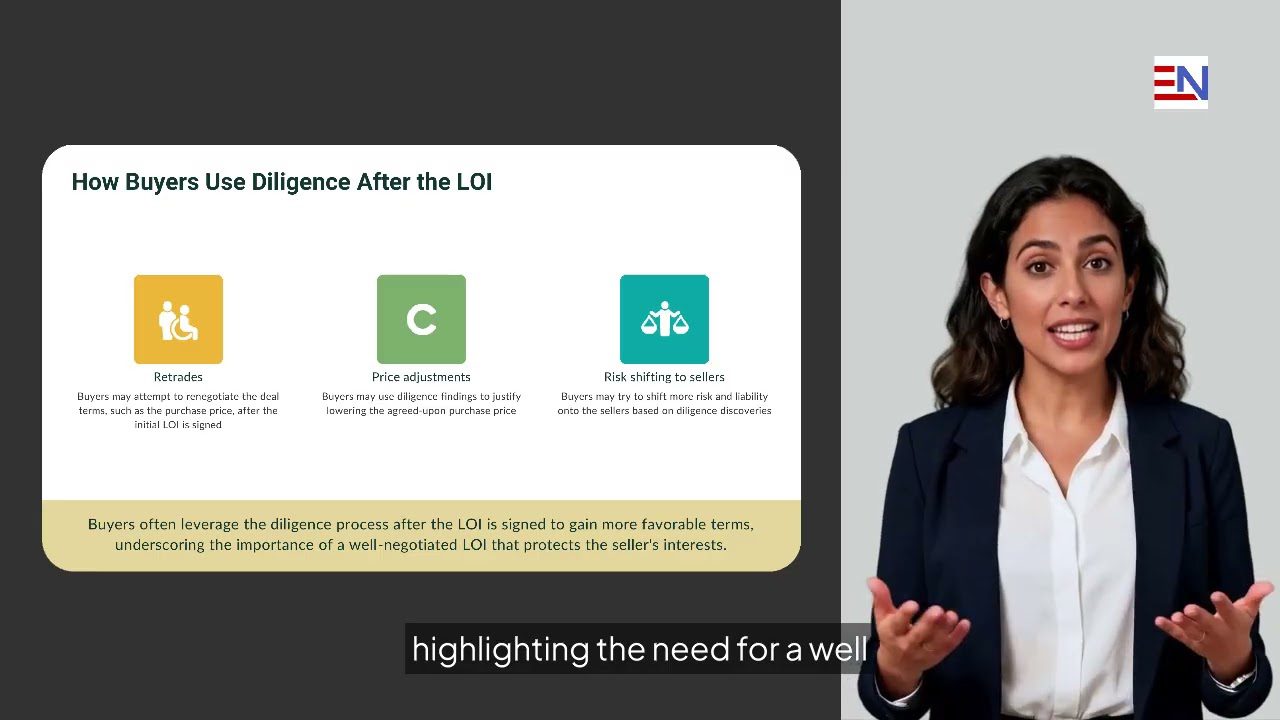

Diligence scope is decided early

The LOI frames what the buyer will examine — financial diligence, legal and compliance review, operational exposure. Sellers tend to read the diligence paragraph passively, as something done to them. It deserves active negotiation, for one reason: after the LOI, diligence becomes the buyer’s primary lever.

The post-LOI pattern is well-worn: diligence findings become retrades, retrades become price adjustments, and adjustments shift risk to the seller — late in the process, when the seller’s alternatives are gone and the cost of saying no has tripled. A defined diligence scope with a defined timeline does not prevent findings, but it prevents the open-ended fishing expedition that manufactures them.

Employment and covenants start here

Two categories of post-closing terms routinely enter the deal at the LOI stage and harden from there.

Employment terms — length of post-closing employment, compensation assumptions, termination expectations. The single sentence “Seller to remain for three years at mutually agreeable compensation” is a framework the seller will live inside; “mutually agreeable” is not a number, and the seller’s leverage to make it a good number is highest now.

Restrictive covenants — non-competes, non-solicits, and their geographic and time scope are frequently previewed in the LOI. A seller who lets “standard non-compete” pass unexamined at this stage will be negotiating the definition of standard from a much weaker position at the document stage.

Red flags sellers miss

Three patterns in LOI drafting reliably signal trouble ahead: vague language where economics should be specific (“approximately,” “subject to adjustment,” “to be determined”); buyer discretion clauses that let the buyer unilaterally modify scope, timeline, or conditions; and open-ended diligence with no defined endpoint, which functions as a perpetual option on the practice at the seller’s expense.

None of these requires a hostile buyer to do damage. They simply move every future disagreement onto the buyer’s terrain.

When to push back — and when not to

Not every term deserves a fight, and a seller who contests everything spends credibility needed for the terms that matter. The framework: push hard on economic certainty (price structure, exclusivity scope, diligence definition, covenant scope — the terms that cannot be fixed later), and concede strategically on process terms that keep deal flow moving. Protecting the downside outranks improving the upside; a slightly better price inside a badly structured LOI is a bad trade.

This is also the moment for counsel — not after the LOI is signed. A seller-protective LOI has clear economics, defined diligence, and balanced exclusivity, and the difference between that document and the buyer’s first draft is typically a few days of negotiation while the seller still has the leverage to win the points. Counsel brought in afterward spends the rest of the transaction managing problems that were negotiable once.

What a seller-protective LOI contains

Translated into drafting terms, a seller-protective LOI does six specific things.

It states the economics with numbers, not adjectives — purchase price, structure, the cash portion at closing, and any rollover or contingent component with its essential terms, so “subject to adjustment” cannot quietly absorb six figures later. It defines diligence — scope, document categories, and a completion deadline. It bounds exclusivity — a defined period, sized to the diligence timeline, ideally with milestones that end it early if the buyer stalls. It previews the covenants — the geographic radius and duration of any non-compete, stated rather than deferred. It frames post-closing employment with at least the term and the compensation basis, so “mutually agreeable” has an anchor. And it allocates costs if the deal dies — who paid for what, resolved in advance rather than litigated in resentment.

None of this makes an LOI adversarial. It makes the LOI do its actual job: recording what the parties agreed while they were still agreeing. Buyers with genuine intent rarely resist specificity; the ones who do are telling the seller something useful early, at the only price the information will ever be available for — nothing.

The takeaway

The LOI is not the beginning of the paperwork; it is the end of the leverage. Sellers who negotiate it as the real agreement — specific economics, bounded exclusivity, defined diligence, examined covenants — carry their leverage into diligence instead of surrendering it at the threshold.

The full webinar deck, The Letter of Intent in Dental Practice Sales, is available as a PDF download.

If you have an LOI in hand — or expect one soon — having it reviewed before signing is one of the highest-leverage moves available to a seller. Conversations are confidential and focused on your specific goals. Schedule a confidential consultation.

This article is for informational purposes only and is not legal advice. No attorney-client relationship is formed by reading it.