Most dental practice acquisitions do not fail at the negotiating table. They fail quietly, months after closing, when the EBITDA turns out to have been optimistic, a key associate leaves, or a compliance issue surfaces that diligence never reached. The buyer who was focused on growth and speed in March is focused on damage control in November.

This article covers where buyers actually get burned in dental acquisitions — and the specific decisions, made before closing, that determine whether problems surface as negotiating points or as losses.

Why buyer risk is underestimated

Buyers, especially first-time buyers and fast-moving expansion buyers, tend to underestimate acquisition risk for a simple reason: the risks are not visible at the stage where most of the attention gets paid. The letter of intent and the headline price absorb the energy. Diligence and deal structure — where the real risk lives — feel like process.

But risk hides in exactly those two places. It hides in what diligence does not examine, and it hides in how the purchase agreement allocates problems that surface later. A buyer who treats diligence as a formality and the asset purchase agreement as paperwork has, in effect, agreed to absorb whatever the seller’s practice turns out to contain.

The discipline that protects buyers is unglamorous: slow down at the right moments, ask for the right documents, and structure the economics so that late discoveries have a remedy other than litigation.

The myth of seller representations

The most common false comfort in dental acquisitions is the belief that seller representations and warranties function as insurance. The reasoning goes: the seller represented that the financials are accurate and the practice is compliant, so if that turns out to be wrong, the buyer has a claim.

Technically true. Practically, three problems.

First, enforcement is expensive. Pursuing a claim under seller reps means a legal process measured in months or years, with uncertain outcomes and legal fees that erode whatever recovery is available.

Second, recovery is limited. Even a successful claim runs into the practical question of collecting from a seller who may have already spent, invested, or protected the proceeds.

Third, a lawsuit does not fix the practice. If the hygiene program is unsustainable or the associate non-competes are unenforceable, a judgment against the seller does not restore the revenue.

Representations matter — they set the baseline for what the buyer was promised, and they support the remedies that do work, like escrows and holdbacks. But they are the backstop, not the protection. The protection is finding the problem before closing.

Where buyers actually lose money

Across dental transactions, buyer losses concentrate in three areas.

Overstated EBITDA. The seller’s earnings number is the foundation of the price, and it is routinely built on adjustments — add-backs for owner compensation, one-time expenses, personal items run through the business. Buyers who accept the adjusted number without validating it against actual cash collections are negotiating from the seller’s spreadsheet, not from the practice’s reality.

Compliance failures. Corporate practice of dentistry rules, supervision and delegation requirements, and documentation standards are easy to under-examine because they do not show up in the financials. They show up afterward — as exposure the buyer now owns.

Staff and associate instability. The practice’s value walks out the door every evening. Compensation misalignment, weak or unenforceable associate non-competes, and post-closing turnover risk are routinely underweighted in diligence, and they are among the most expensive problems to discover after the transition.

Financial diligence blind spots

Three financial questions deserve more attention than they usually get.

Collections versus production. Dental practices report production — the value of work performed — but the buyer is buying collections, the cash that actually arrives. The gap between the two reflects write-offs, payor adjustments, and billing practices. A practice with strong production and weak collections is a different asset than its profit-and-loss statement suggests.

Hygiene sustainability. A practice that depends on a high-volume hygiene program is dependent on the hygienists who run it. In a labor market where hygiene staffing is tight, revenue built on hygiene volume deserves a staffing-risk discount that sellers rarely volunteer.

Payor mix assumptions. Revenue quality depends on who is paying. A shift in payor mix — including the growing weight of corporate insurance networks — can erode revenue without any change in patient volume. Diligence should test whether the current mix is stable and what the trend has been, not just what the latest year shows.

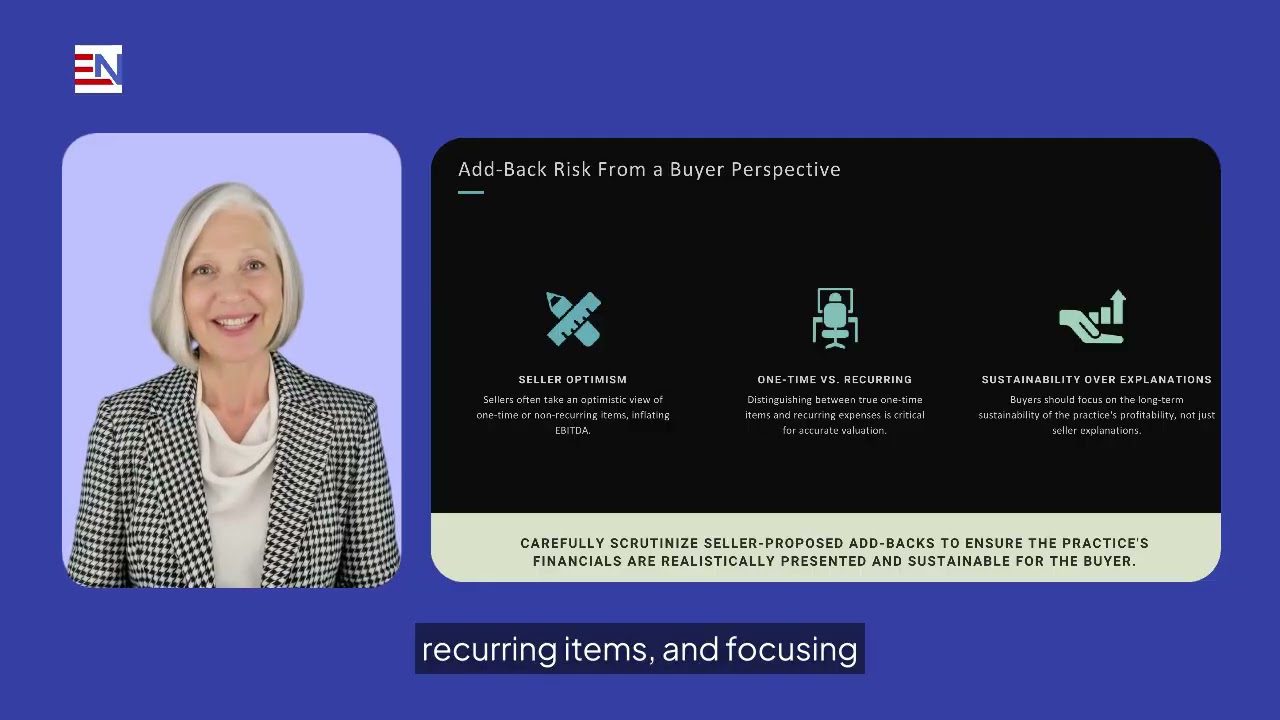

Add-backs from the buyer’s side

Sellers present add-backs optimistically; that is their role. The buyer’s role is to distinguish between adjustments that reflect genuine buyer-run economics and adjustments that reflect hope.

The dividing line is sustainability. A documented, verifiable, one-time expense is a legitimate add-back. A recurring expense recharacterized as one-time is not. The test is not whether the seller can explain the adjustment — sellers can explain everything — but whether the earnings survive the adjustment under new ownership, on a sustained basis.

Buyers who hold this line do more than protect the price. They learn how the seller thinks, which is useful information for every other open issue in the deal.

Compliance risks buyers miss

Three compliance areas deserve specific attention in dental diligence.

Corporate practice of dentistry. State rules restrict who may own a dental practice and how non-dentists may participate in its economics. Structures that drift across that line — sometimes inadvertently, over years — create liability the buyer inherits.

Supervision and delegation. The procedures performed by hygienists and assistants are governed by state supervision and delegation requirements. Practices develop informal habits; informal habits become compliance exposure precisely when ownership changes and someone finally looks.

Incomplete compliance programs. Many practices run on undocumented, informal compliance — no written policies, no training records, gaps in required documentation. The absence of a problem on paper is not the absence of a problem.

The LOI mistakes that hurt buyers

Buyer leverage peaks before the letter of intent is signed and declines steadily afterward. Three LOI mistakes spend that leverage badly.

Vague diligence rights. If the LOI does not define what the buyer may examine and on what timeline, the buyer will negotiate for access while exclusivity runs and momentum builds toward closing.

Over-broad seller discretion. The LOI should restrict what the seller may change during diligence — hiring, contracts, compensation, equipment. A seller free to make operational changes during the deal can hand the buyer a different practice at closing than the one that was priced.

Poorly structured economics. Purchase price adjustments, holdbacks, and contingent payments defined loosely at the LOI stage become disputes at the document stage — when revisiting them costs leverage the buyer no longer has.

Structuring real protection

Buyer protection that actually works is structural, agreed before closing.

Escrows and holdbacks. A portion of the purchase price held back for a defined period is the most practical remedy for post-closing discoveries. It converts “sue the seller” into “claim against the escrow” — a different proposition in cost, speed, and likelihood of recovery.

Indemnity terms with teeth. Caps, baskets, and survival periods determine what the seller actually stands behind. These are negotiated numbers, and they should reflect the specific risks diligence identified, not a form document’s defaults.

Walk-away rights. The buyer should retain a defined right to terminate if diligence surfaces material problems. A buyer who cannot walk away cannot negotiate.

Why speed destroys value

Sellers and brokers create urgency; that is how deals maintain momentum. But three speed-driven failures account for a disproportionate share of buyer losses: deal fatigue that produces rushed decisions late in the process, compressed timelines that force diligence shortcuts, and false urgency that pressures buyers into waiving the review that would have caught the problem.

The buyer’s advantage is that almost no dental deal is actually as time-sensitive as it is presented to be. A buyer who holds the diligence line rarely loses the deal over it — and a seller who would rather lose the deal than allow diligence has answered the most important diligence question already.

What a buyer-protective deal looks like

A well-structured dental acquisition has three signatures: a price built on sustainable, buyer-verified EBITDA rather than seller projections; risk allocation that is explicit, with indemnity, escrow, and holdback structures matched to the risks diligence actually found; and protections drafted to be specific, measurable, and practically enforceable.

None of this slows a deal down meaningfully. It front-loads work that, done late or not at all, costs far more.

The takeaway

Buyers get burned in dental acquisitions when growth ambition outruns risk discipline — when reps substitute for diligence, when the seller’s EBITDA substitutes for verification, and when speed substitutes for structure. The fixes are available to every buyer, but only before closing.

The full webinar deck, Buying a Dental Practice: Where Buyers Get Burned — and How to Avoid It, is available as a PDF download.

If you are evaluating a dental practice acquisition — or are already under LOI — early legal guidance can significantly impact outcomes. Conversations are confidential and focused on your specific goals. Schedule a confidential consultation.

This article is for informational purposes only and is not legal advice. No attorney-client relationship is formed by reading it.